On Wednesday, the U.S. dollar index fell in the U.S. pre-session due to CPI data in line with expectations, but then Trump announced that he would resume the “heavy blow” against Iran, the U.S. index continued to rebound and returned to the 100 mark, and eventually closed up 0.09% at 100.04; the benchmark 10-year U.S. bond yield closed at 4.559%, and the 2-year bond yield, which is sensitive to the Fed’s policy rate, closed at 4.158%. The 2-year U.S. bond yield, which is sensitive to Fed policy rates, closed at 4.158%.

Even though the CPI data moderated market expectations for a Fed rate hike, spot gold continued to fall as the U.S.-Iran cease-fire faltered, dropping nearly $200 during the day and eventually closing down 4.46% at $4070.56/oz; spot silver closed down 3.02% at $63.38/oz.

Crude oil opened up in the US pre-market session. WTI crude oil returned above the $90 mark, eventually closing up 3.36% at $92.69/barrel; Brent crude oil eventually closed up 2.88% at $93.74/barrel.

U.S. stocks closed down 1.87% on the Dow, 1.62% on the S&P 500 and 1.98% on the Nasdaq. Super Micro Computer (SMCI.O) fell nearly 28 percent, while Tesla (TSLA.O) and Nvidia (NVDA.O) dropped more than 3 percent. The Nasdaq China Golden Dragon closed down 0.28 percent, with NetEase (NTES.O) up nearly 4 percent and Global Data (GDS.O) down 7 percent.

Month: June 2026

June 10th Market Inventory

On Tuesday, due to the fragile ceasefire situation in the Middle East, the dollar index fell first and then rose, almost showing a “V-shaped trend” during the day, and ultimately closed down 0.04% at 99.95; benchmark 10-year U.S. bond yields closed at 4.522%, the Fed’s policy rate sensitive to the 2-year U.S. bond yields closed at 4.135%.

With market expectations of a Fed rate hike within the year heating up and a U.S. strike on Iran, spot gold fell sharply in the U.S. session, dropping to an intraday low of $4,236.77 during the session, and ultimately closing down 1.63% at $4,260.37 per ounce; spot silver closed down 4.1% at $65.36 per ounce.

Crude oil shook down during the day, but oil prices rebounded briefly after the U.S. crackdown on Iran.WTI crude oil fell below the $90 mark, and once fell to an intraday low of $86.96, then rebounded slightly, and ultimately closed down 2.91% at $89.68/barrel; Brent crude oil ultimately closed down 2.56% at $91.92/barrel.

The three major U.S. stock indexes were mixed, with the Dow closing up 0.17%, the S&P 500 down 0.26%, and the Nasdaq down 0.97%. Maverick Technology (MRVL.O) fell 7.6 percent, Qualcomm (QCOM.O) dropped 5.6 percent and Tesla (TSLA.O) fell 3 percent. The Nasdaq China Golden Dragon Index is down 0.39 percent, with Ideal Motors (LI.O) and Azera Motors (NIO.N) down about 3 percent.

June 9 Market Inventory

On Monday, Iran and Israel agreed to stop attacking each other after a call from President Donald Trump. The U.S. dollar index retreated slightly but still hovered near its highest level in nearly two months, eventually closing down 0.07% at 100.00; the yield on the benchmark 10-year U.S. bond closed at 4.568%, while the yield on the 2-year U.S. bond, which is sensitive to Fed policy rates, closed at 4.166%.

Spot gold fell and then rose, losing the 4300 mark during the session and falling to an intraday low of $4288.01, but recovered all of its intraday losses and turned higher in the U.S. session, eventually closing up 0.05% at $4329.886 per ounce; spot silver was broadly oscillating, eventually closing up 0.4% at $68.15 per ounce.

WTI crude oil rose more than 4% at one point after opening higher, but in the U.S. pre-market session jumped sharply, erasing most of the day’s gains, and finally closed up 0.7% at $92.37 per barrel; Brent crude oil finally closed up 1.52% at $93.42 per barrel.

The three major U.S. stock indexes were mixed, with the Dow closing down 0.16%, the S&P 500 up 0.3% and the Nasdaq up 0.86%. Maverick Technology (MRVL.O) rose 9.6%, Intel (INTC.O) rose 11%, and Micron Technology (MU.O) rose nearly 10%. The Nasdaq China Golden Dragon Index closed down 0.6 percent, with Alibaba (BABA.N) down nearly 1 percent.

June 8 Market Inventory

On Friday, as the U.S. non-farm payrolls data in May again recorded strong growth, which pushed up the market’s expectations for the Federal Reserve to raise interest rates within the year. The U.S. dollar index in the U.S. market before the near straight-line pull up, and surged to the 100 mark, and finally closed up 0.63% at 100.07; benchmark 10-year U.S. bond yields closed at 4.522%, the Fed’s policy rate-sensitive 2-year U.S. bond yields closed at 4.147%.

As the dollar and U.S. bond yields rose, spot gold came under pressure and dived sharply before the U.S. market, once falling to an intraday low of $4,311.78, a big drop of more than $150 from the intraday high, and ultimately closed down 3.3% at $4,327.77 an ounce, retiring all of the year’s gains; spot silver fell below the $70 mark, and ultimately ended up 8.11% lower at $67.88 an ounce.

Oil prices fell on Friday as traders became more and more convinced that another conflict between the U.S. and Iran was becoming less and less likely.WTI crude oil continued to oscillate in the Asian trading session, increased volatility in the European trading session and continued to sink in the U.S. trading session, ultimately closing down 2.92% at $91.73/barrel; Brent crude oil ultimately ended up 2.48% lower at $92.03/barrel.

U.S. stocks closed down 1.35% on the Dow, 2.64% on the S&P 500, and 4.18% on the Nasdaq, with the S&P 500 posting its biggest one-day drop since October 2025; and the Nasdaq posting its biggest one-day drop since April 2025. Most of the semiconductor sector fell, the Philadelphia Semiconductor Index late in the trading session to extend the decline to 10%, the largest single-day decline since April 2025. NVIDIA (NVDA.O) fell more than 6 percent, TSMC (TSM.N) dropped 6.68 percent, Broadcom (AVGO.O) fell nearly 8 percent and Intel (INTC.O) fell more than 11 percent. The Nasdaq China Golden Dragon Index closed down 3.56%, with Pony Intelligence (PONY.O) down 9.83%, Baidu (BIDU.O) down 9.75%, and Kingsoft Cloud (KC.O) down 6.70%.

Black Friday plays out as tech, chips, and midcaps go down across the board

June 5 closing, the three major U.S. stock indexes all closed down, the Dow Jones fell 1.35%, at 50,866.78 points, the S&P 500 plunged 2.64%, at 7,383.74 points, the Nasdaq closed at 25,709.43 points.

From the weekly performance point of view, the Dow closed down slightly 0.32%, the S&P retreated 2.59% for the whole week, and the Nasdaq plunged 4.68% in a single week, within a week, the U.S. stock bulls suffered back-to-back blows.

The leading U.S. technology stocks went out collectively, and none were spared. Tesla, Nvidia fell more than 6%, Meta plunged more than 5%, Amazon fell more than 3%, Microsoft, Apple, Google in turn weakened, once held up the U.S. stock market bull market hugging plate, become the first choice of capital sell-off.

The most tragic when the chip track, Philadelphia Semiconductor Index single day wildly fell 10.26%, hit a stage of rare plunge. Mai Weir Technology plunged more than 16% to lead the market, Micron, ARM fell nearly 13%, Intel, Qualcomm, AMD synchronized plunge of more than 11%, Broadcom fell nearly 8%, TSMC dipped more than 6%, the semiconductor industry chain rout.

Chip crash collapsed along the way with the collapse of the optical communications sector, Nokia fell more than 13%, Coherent, Corning fell more than 10%, Lumentum fell more than 8%.

Panic quickly spilled over and spread to the Chinese market, the Nasdaq China Golden Dragon Index fell 3.54% in a single day. Atlas Solar plunged nearly 12%, Pony Intelligence nearly 10% down, Baidu, CenturyLink, JinkoSolar fell more than 9%, Wo Sai technology, Kingsoft cloud fell equally high.

The stock market is wailing at the time, precious metals failed to carry the flag of hedge.

Gold fell in a single day after the week fell to 5.21%, silver plunged 10.39% in a single week, gold and silver synchronized weakness.

Weekly Hot Pick: Strong Nonfarm Payrolls Stimulate Rate Hike Expectations for the Year, Global Central Banks Resume Gold Purchases in April

This week’s dollar index overall shock upward, after the release of Friday’s big more than expected non-farm payrolls data, the market on the Federal Reserve rate hike within the year is expected to warm up sharply, the U.S. index briefly higher to 99.6.

Spot gold this week’s shock adjustments, non-farm payrolls released once below $4400 / ounce, is expected to be the fourth consecutive weekly close down. The U.S. dollar and U.S. bond yields stabilized at the stage, geopolitical news, although it helps to boost safe-haven demand, but the overall risk appetite back up to limit the safe-haven gold prices unilateral upward.

Silver overall trend and gold convergence but slightly stronger volatility, the lowest down to 70.8 U.S. dollars / ounce near the mid-week.

International crude oil edged higher this week and is expected to record its first close in three weeks. Volatility was largely driven by expectations of geopolitical moderation, shipping and inventory data, with easing risk aversion weighing on risk aversion-pushed oil price premiums. There were no clear signals of tightening in supply/demand fundamentals, making it difficult for crude to extend its previous swift gains.

Non-U.S. currencies generally relative to the dollar to maintain narrow fluctuations, the euro, the pound against the dollar range shock is dominated by the yen, the most pressure, the dollar against the yen touched 160 near many times, the market is once again concerned about whether the Japanese authorities to intervene.

U.S. stock market, this week, the performance of the main U.S. stock index differentiation, the Dow refreshed the historical closing highs, the S&P 500 rose slightly, Nasdaq slightly under pressure, the technology sector within the rotation is obvious. Representative dissident stocks, chip giant Broadcom due to the earnings outlook is less than expected significant decline.

June 5 Market Inventory

On Thursday, due to market optimism about the cease-fire in Lebanon, the dollar index fell from nearly two-month highs, but in the U.S. market showed a “V rebound”, and ultimately closed down 0.09% at 99.44; the benchmark 10-year U.S. bond yields closed at 4.481%, sensitive to the Federal Reserve’s policy rate of the 2-year U.S. bond yields were closed at 4.049%.

As the dollar and U.S. bond yields fell, spot gold rebounded, once during the session above $4,510, but failed to stabilize here, and ultimately closed up 0.94% at $4,475.58 per ounce; spot silver ultimately closed up 1.6% at $73.87 per ounce.

Crude oil plunged more than 3% during the day due to increased market optimism.WTI crude oil jumped sharply in the European trading session, then fell into shock near $93, and finally closed down 3.48% at $94.49/barrel; Brent crude oil finally closed down 3% at $94.37/barrel.

The U.S. Dow closed up 1.73% and hit a new closing high, the S&P 500 gained 0.41%, and the Nasdaq Composite edged lower. NVIDIA (NVDA.O) rose nearly 2%, Micron Technology (MU.O) fell 7.7% and Broadcom (AVGO.O) dropped more than 12%. The Nasdaq China Golden Dragon Index closed down 0.6%, while Xiaopeng Auto (XPEV.N) fell 3.5%.

June 4 Market Inventory

On Wednesday, due to the diplomatic negotiations between Iran and the United States is still in a stalemate, the dollar index continued upward momentum, and eventually closed up 0.33%, at 99.53, for the third consecutive day of gains; benchmark 10-year U.S. bond yields closed at 4.500%, the Federal Reserve’s policy rate sensitive to the 2-year U.S. bond yields closed at 4.086%.

Because the market concerns about inflation, and “small non-farm payrolls” data exceeded the expectations of the market inhibit the Federal Reserve rate cuts within the year is expected, spot gold shocked downward during the day, the plate once fell below 4430 U.S. dollars, a big drop of nearly 70 U.S. dollars from the high point, and finally closed down 1.21%, at 4433.95 U.S. dollars / ounce; spot silver finally closed down 3.21% at $72.71/oz.

Due to the stalemate in the U.S.-Iran negotiations and the outbreak of new conflicts in the Gulf region, crude oil rose for the third consecutive trading day. WTI crude oil once surged to $98 during the session, but failed to stabilize here, and finally closed up 2.77% at $97.90/barrel; Brent crude oil finally closed up 2.18% at $97.29/barrel.

The three major U.S. stock indexes closed lower, with the Dow closing down 1.21%, the S&P 500 down 0.74%, and the Nasdaq down 0.89%. Microsoft (MSFT.O) and Nvidia (NVDA.O) both fell more than 3%, Oracle (ORCL.N) fell more than 5%, and Intel (INTC.O) rose 4%. The Nasdaq China Golden Dragon Index closed down 2.46%, with Alibaba (BABA.N) down more than 2%.

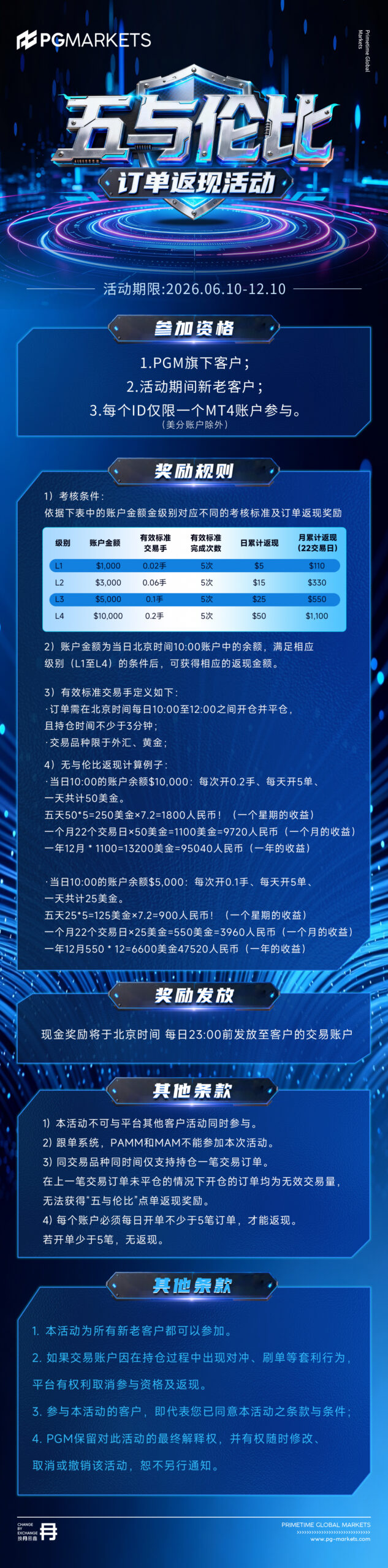

“Five with Lundby” Order Rebate Program

June 3 Market Inventory

On Tuesday, investors were cautious about news of progress toward ending the U.S.-Israeli war against Iran, despite numerous market rumors about U.S.-Iranian negotiations. The U.S. dollar index fell and then rose, but remained firmly above the 99 mark, and eventually closed up 0.01% at 99.20; the benchmark 10-year U.S. bond yield closed at 4.446%, and the 2-year U.S. bond yield, which is sensitive to the Fed’s policy rate, closed at 4.051%.

Spot gold surged above $4,540 in European trading, but then gave back most of the day’s gains and fell below the $4,500 mark, eventually closing up 0.09% at $4,488.23 per ounce; spot silver ended up 0.4% higher at $75.12 per ounce.

WTI crude oil fell before rising, and then opened up in the U.S. trading session, ending up 0.86% higher at 95.23 USD/barrel; Brent crude oil finally closed up 0.26% at USD 95.21/barrel.

U.S. stocks Dow closed up 0.45%, the S&P 500 index rose 0.13%, the Nasdaq rose slightly. Microsoft (MSFT.O) fell 4%, Google (GOOG.O) dropped nearly 4%, and Myvell Technology (MRVL.O) jumped 32% after Jen-Hsun Huang said Myvell Technology would be the next trillion-dollar company. The Nasdaq China Golden Dragon Index closed up 1.8%, with Alibaba (BABA.N) up more than 4%.